Once you have paid off your debt and have a strong Emergency Fund, you can start aggressively paying down your mortgage. Here are afew ways that may help you pay your mortgage.

Education Goals

-

Round Up Your Payments

-

Refinance Your Mortgage

-

Bi-Weekly Payments

-

Make Lump-Sum Payments

-

Track Your Mortgage

Week 5.1: Education Goals by Hellen Lovato

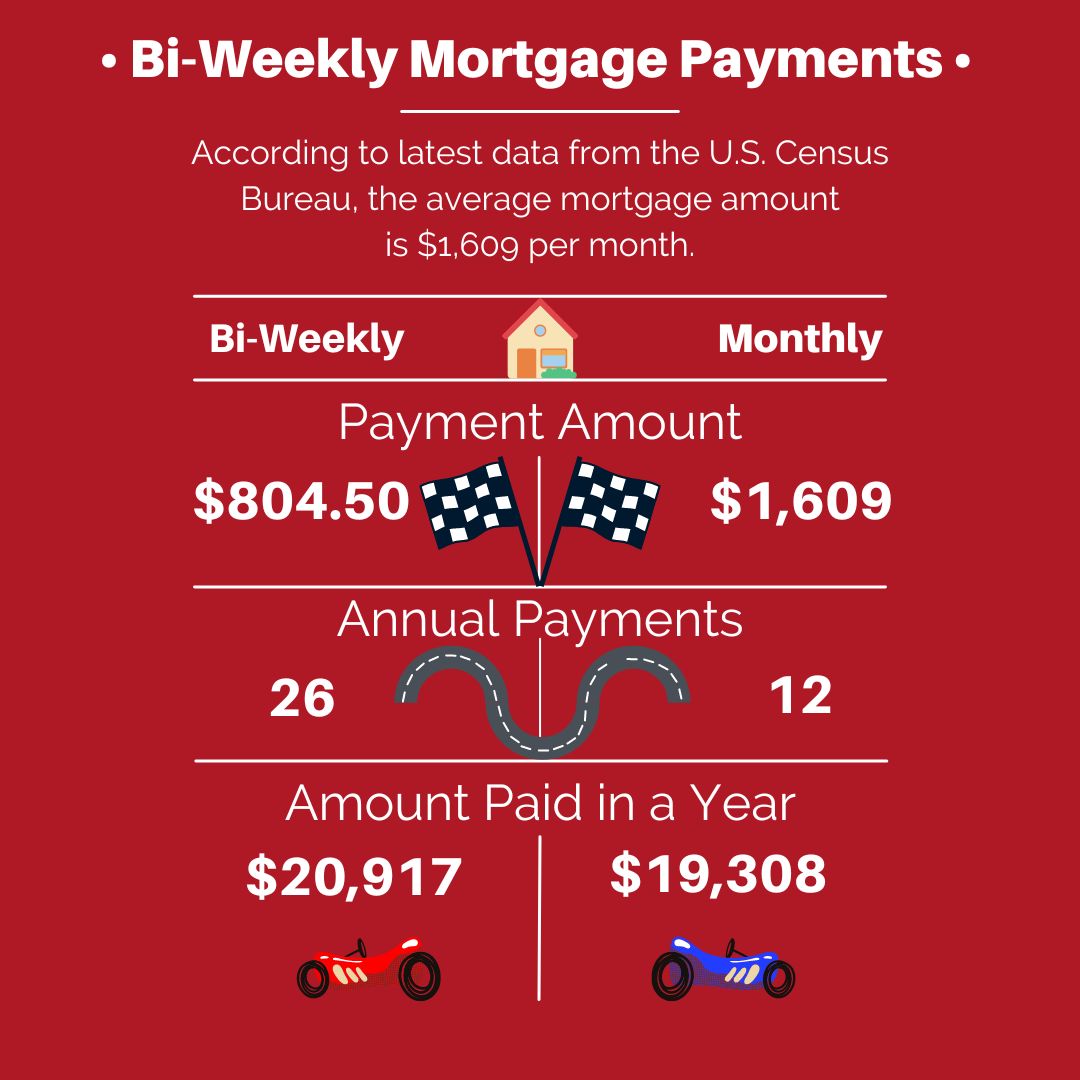

Bi-Weekly Payments

One of the most popular ways to pay down your mortgage is by making bi-weekly payments instead of one lump-sum every month.

A biweekly mortgage means that you would be paying every two weeks, or 26 half payments. This results in 13 full payments over a 12-month period, accelerating the payoff of the mortgage.

The extra payment per year can provide significant savings in total interest over the life of the mortgage.

According to latest data from the U.S. Census Bureau, the average mortgage amount is $1,609 per month.

Week 5.2: Bi-Weekly Payments by Hellen Lovato

Let’s use that number in an example on how bi-weekly payments works.

If you make a $1,609 payment a month, that is 12 payments a year, equals to $19,308. If you make by-weekly payments of $804.50 for a year that will equal to 26 payments a year. In a year you would have paid $20,917, which is equivalent to13 full payments.

Before you start making bi-weekly payments make sure your mortgage company accepts biweekly payments without charging you fees.

Make Lump Sum Payments

If your mortgage company allows it, make lump sum payments towards your principal every now and then. Whenever you get a sudden windfall of money, a bonus, or a raise put it towards your principal.

Remember, you can send in an extra mortgage payment every month, but you’ll still be required to make a mortgage payment the following month. What changes is that you’ll pay off your mortgage sooner, and you’ll save money on interest.

Make sure that your mortgage doesn’t charge prepayment penalties before making a lump-sum payments.

Week 5.3: Make Lump-Sum Payments by Hellen Lovato

Round Up Your Payments

By rounding your mortgage loan up to the next whole-dollar increment can bring big savings, simply, easily and painlessly on your budget.

Let’s say paying $1,000 instead of $955 each month, the $45 more you are paying will come directly off the Principal amount you owe!

You probably won’t notice the difference in your day-to-day expenses, but over the lifetime of your loan, the extra money will make a huge difference in decreasing your principal balance and save you interest.

Paying an extra $45 per month adds up to $540 per year, this decreases the amount you owe on, and shave off months if not years off your mortgage.

Make sure that your mortgage company doesn’t charge prepayment penalties before making payments.

Week 5.4: Round Up Your Payments by Hellen Lovato

Refinance Your Mortgage

Refinancing can allow you to change the terms of your mortgage to secure a lower monthly payment, switch your loan terms, consolidate debt or even take some cash from your home’s equity to put toward bills or renovations.

Consult with a financial adviser to see if refinancing is beneficial for you.

Week 5.5: Refinance Your Mortgage by Hellen Lovato

Track Your Mortgage

Remember there are no constants in life. Your enviroment, perspectives, job, and attitudes can change as years go by. This is why a regular review of your goals and tracking is critical to make sure that you are on the right track.

The time and effort you put into setting and sticking to your financial goals pays off when you are able to achieve financial independence. No matter your age or what your earning capacity is at this moment, identifying and developing your goals with a rational perspective is critical to your and your family’s future.

Don’t hesitate to use our helpful trackers at the bottom of the page!

Week 5.6: Track Your Mortage by Hellen Lovato

YOU GOT THIS!

This information is meant for educational purposes only and is not intended as financial advice.

![]()

![]()

Financial Wellness Resources & Tools For Debt Elimination